The 2012–2013 Cypriot financial crisis is a major economic

crisis in the

Republic of Cyprus that involves the exposure of Cypriot banks to

the

Greek Debt Crisis, the downgrading of the Cypriot economy to junk

status by international

rating agencies, the consequential inability to refund its state

expenses from the international markets[1][2]

and the reluctance of the government to restructure the troubled Cypriot

financial sector.[3]

On 25 March 2013, a €10 billion bailout was announced in return for

Cyprus agreeing to close its second largest bank, the

Cyprus Popular Bank (also known as Laiki Bank), levying all

uninsured deposits there, and possibly around 40% of uninsured deposits

in the Bank of Cyprus (the Island's largest commercial bank), many held

by wealthy citizens of other countries, significantly Russia, who use

Cyprus as a

tax

haven.[4][5]

All

insured deposits of 100,000 Euros or less will not be affected.[6][7]

Precursors

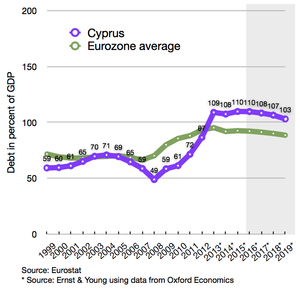

Cyprus's debt percentage compared to Eurozone average since

1999

Following the United States'

subprime mortgage crisis in 2007-2008, which led to a domino effect

of negative consequences in the global economy, the Cypriot economy

contracted by 1.67% in 2009,[8]

largely due to a sharp fall in its tourist and shipping sectors.[9]

Following the contraction, Cyprus experienced continuous increasing

unemployment,[10]

and thus entered into a recession. From 2010 to 2012 the economic growth

of the country has been weak, meaning that the Cypriot economy has yet

to recover to its pre-2009 condition.[8]

Increasing unemployment contributed to an increasing state debt as

expenditure on unemployment benefits kept increasing. Following the

decision of the European Union for a

haircut upwards of 50% on Greek bonds in 2011[11][12],

in which Cypriot banks had invested heavily, the Cypriot financial

system was unable to absorb the cost. The disproportionate size of the

financial sector in relation to the rest of the Cypriot economy meant

that a possible collapse of the Cypriot banks would have catastrophic

results for the economy. The Cypriot state, unable to raise liquidity

from the markets to support its financial sector, requested a bailout

from the European Union.[9]

In September 2011, the credit rating of

Cyprus

was downgraded by all major credit rating agencies following the

Evangelos Florakis Naval Base explosion in July 2011, which occurred

within a period of slow progress for the fiscal and structural reforms.

At the same time yields on its long-term bonds rose above 12%. Despite

its low population and small economy, Cyprus has a large

off-shore banking industry that was shaken to its foundations during

the financial turmoil. With a total

nominal GDP of €19.5bn ($24bn)[13]

the country was unable to stabilize its banks, which had amassed €22

billion of Greek private sector debt and were disproportionately hit by

the

haircut taken by creditors. According to reports in the magazine

Newsweek bank deposits from

Russian

business corporations total $60bn out of a total deposits of $120bn. The

situation is also compounded by the fact that Russian oligarch

Dmitry Rybolovlev owns a 10% shareholding of

Bank of Cyprus.[14][15][16]

A report published in April 2012 by a team of 16 Cypriot economists,

organized by the citizens group Eleutheria ("Freedom"),[17]

attributes the causes of the crisis to sliding competitiveness and also

to increasing public and private debt, which were both exacerbated by

the banking crisis.[18]

Emergency

loan (2012)

Since January 2012, Cyprus has been relying on a €2.5bn (US$3.236

billion) emergency loan from Russia to cover its budget deficit and

re-finance maturing debt. The loan has an interest rate of 4.5% and it

is valid for 4.5 years.[19][20]

It was originally expected that Cyprus would be able to fund itself

again by the first quarter of 2013.[20]

Credit rating downgrade (mid 2012)

On 13 March 2012,

Moody's slashed Cyprus's

credit rating to Junk status, warning that the Cyprus government

would have to inject more fresh capital into its banks to cover losses

incurred through Greece's debt swap. On 25 June 2012, the day when

Fitch downgraded bonds issued by Cyprus to BB+, which disqualified

them from being accepted as collateral by the

European Central Bank, the Cypriot government requested a

bailout

from the

European Financial Stability Facility or the

European Stability Mechanism.[16]

Request for EU intervention and agreement

The Cypriot Government was reported requesting a bailout from the

European Financial Stability Facility or the

European Stability Mechanism on 25 June 2012, citing difficulties in

supporting its banking sector from the exposure to the Greek debt.[21]

Representatives of the Troika (the

European Commission, the

International Monetary Fund, and the European Central Bank) arrived

to the island in July to investigate the country's financial problems,

and submitted the terms of the bailout to the Cypriot government on 25

July.[22]

The Cypriot government expressed disagreement over the terms, and

continued negotiation with Troika representatives concerning possible

alterations to them throughout the following months.[23][24]

On 20 November, the government handed its counter-proposals to the

Troika on the terms of the bailout,[25]

with negotiations continuing. On 30 November it was reported that Troika

and the Cypriot Government had agreed on the bailout terms with only the

amount of money required for the bailout remaining to be agreed upon.[26]

The bailout terms were made public on 30 November.[27]

The

austerity measures included cuts in civil service salaries, social

benefits, allowances and pensions and increases in VAT, tobacco, alcohol

and fuel taxes, taxes on lottery winnings, property, and higher public

health care charges.[28]

Eurozone/IMF deal

On 16 March 2013, the

European Commission (EC),

European Central Bank (ECB) and

International Monetary Fund (IMF) agreed a €10 billion deal with

Cyprus,[29]

making it the fifth country—after Greece, Ireland, Portugal and Spain—to

receive money from the EU-IMF. As part of the deal, a one-off

bank deposit levy of 6.7% for deposits up to €100,000 and 9.9% for

higher deposits, was announced on all domestic bank accounts. Savers

were due to be compensated with shares in their banks.[30]

Measures were put in place to prevent withdrawal or transfer of moneys

representing the prescribed levy.[31]

The deal required the approval of the

Cypriot parliament, which was due to debate it on 18 March.

According to President

Nicos Anastasiades, failure to ratify the measures would lead to a

"disorderly bankruptcy" of the country.[30]

The Russian government "blasted Cyprus's bank levy, piling more pressure

on [capital city] Nicosia" ahead of the parliament's vote on the

bailout. Russia had not decided at the time whether to extend its

existing loan to Cyprus.[32]

With the background of large demonstrations outside the House of

Representatives in Nicosia by Cypriot people protesting the bank deposit

levy,[33]

the deal was rejected by the Cypriot parliament on 19 March 2013 with 36

votes against, 19 abstentions and one not present for the vote.[34]

On 22 March, the Cyprus legislature approved a plan to restructure

the

Cyprus Popular Bank, its second largest bank also known as

Laiki Bank, creating in the process a so-called "bad

bank."[35]

On 25 March, Cyprus President Anastasiades,

Eurozone finance ministers, and IMF officials announced a new plan

to preserve all

insured deposits of 100,000 Euros or less without a levy, but shut

down Laiki Bank, levying all uninsured deposits there, and levying 40%

of uninsured deposits in Bank of Cyprus, held mostly by wealthy Russians

and Russian

Multinational corporations who use Cyprus as an

offshore bank and safe

tax

haven. The revised agreement, expected to raise 4.2 billion Euros in

return for a €10 billion bailout, does not require any further approval

of the Cypriot parliament, as the legal framework for the implied

solutions for Laiki Bank and Bank of Cyprus has already been accounted

for in the bill passed by the parliament last week.[6][7]

When the final agreement was settled on 25 March, the idea of

imposing any sort of deposit levy was dropped, as it was instead now

possible to reach a mutual agreement with the Cypriot authorities

accepting a closure for the most troubled

Laiki Bank (with remaining good assets and deposits below €100,000

being saved and transferred to

Bank of Cyprus, while shareholder capital would be written off, and

uninsured deposits above €100,000, along with other creditor claims,

would also be lost to the degree being decided by how much the

receivership subsequently can rescue out from liquidation of the

remaining bad assets), and as an extra safety measure uninsured deposits

above €100,000 in Bank of Cyprus will also remain frozen until a

recapitalisation has been effected (with a possible imposed haircut if

this is later deemed necessary to reach the aim for a 9%

tier 1 capital ratio). The targeted closure of Laiki and the

recapitalisation plan for Bank of Cyprus helped significantly to reduce

the needed loan amount for the overall bailout package, so that €10bn

was still sufficient without need for imposing a general levy on bank

deposits. Final conditions for activating the programme for the Cypriot

bailout package will be outlined by the Troika's

MoU agreement in early April 2013, and will include:[36]

|

“ |

- Recapitalisation of the entire financial sector while

accepting a closure of the Laiki bank,

- Implementation of the

anti-money laundering framework in Cypriot financial

institutions,

- Fiscal consolidation to help bring down the Cypriot

governmental budget deficit,

- Structural reforms to restore competitiveness and

macroeconomic imbalances,

- Privatization programme.

|

” |

According to IMF, the Cypriot debt-to-GDP ratio is on this background

now forecasted only to reach 100% in 2020, and thus remain within

sustainable territory.[37]

Given the proposed and actual element of taking deposits as part of

the agreement, it was sometimes referred to as a "bail-in" rather than a

bailout.[38]

Irish MEP

Nessa Childers, daughter of the country's former President

Erskine H. Childers, painted a bleak picture. She described the

efforts of the EU-IMF as an "incompetent mess" and said the Eurozone was

more destabilised as a result.[39]

Cypriot

public reactions

Cyprus has seen a number of reactions and responses towards the

austerity measures of the bailout plan. On 8 November 2012,

ERAS (Committee for a Radical Leftist Rally, Επιτροπή για μια

Ριζοσπαστική Αριστερή Συσπείρωση) organised the first protest

against austerity and the Troika negotiations that were still taking

place.[40]

Protesters were gathered outside the

House of Representatives holding banners and shouting slogans

against austerity. Leaflets with alternative proposals for the economy

were distributed in the protest, with proposals including the

nationalization of banking, the reduction of the army and the freezing

of the army budget, and the increase of the corporate tax. Members of

the

New Internationalist Left (NEDA) also participated in the protest.[41]

On 14 November the

New Internationalist Left organised an anti-austerity protest

outside the Ministry of Finance in Nicosia together with the Alliance

Against the Memorandum. In the protest NEDA gave out leaflets, which

expressed the view that "the EU is trying to burden the workers with the

debts from the collapse of the bankers" and that "if this happens, the

Cypriot economy and the future of the new generations will then be

mortgaged to local and foreign profiteers and usurious bankers".[42]

Contract teachers protested outside the House of Representatives on

29 November against austerity measures that would leave 992 of them

without a job next year. The teachers stormed the building and bypassed

the policemen, entering the parliament. The teachers shouted against the

banks and poverty.[43]

A protest by investors was staged on the morning of 11 December outside

the House of Representatives, with protesters again storming parliament

and bypassing the police. The storming of the parliament led to the

interruption of the discussions of the parliamentary committee of

customs. The protesters were asked to leave so that the committee could

continue its work, and the protesters left half an hour later.[44]

A number of protests took place on 12 December. Members of large

families protested outside the House of Representatives against cuts in

the benefits given by the state to support large families. Protesters

threw eggs and stones at the main entrance of the parliament, and a

number of protesters tried to enter the building, but were blocked by

the police force that arrived to handle the protest. It was reported

that a woman fainted during the incidents. The protesters shouted for

the MPs to come out but no response was given.[45]

The protesters were joined by members of KISOA (Cypriot Confederation

of Organisations of the Disabled, Κυπριακή Συνομοσπονδία Οργανώσεων

Αναπήρων), who marched from the Ministry of Finance to the House of

Representatives to protest against cuts in benefits for people with

disabilities.[46]

Later in the day members of public school teachers' trade unions

protested outside the Ministry of Finance against the cuts in education

spending which could result in the firing of teachers.[47]

The unions staged another protest the next day near the House of

Representatives.[48]

See also